Market Update January – March 2018

A Steady Start To 2018

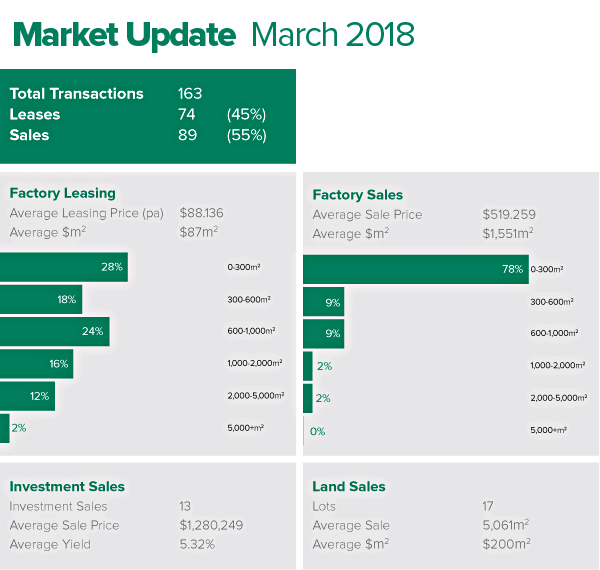

Following a slower than normal start to the year the pace quickened throughout the quarter culminating in 163 transactions which could best be described as a steady start to 2018.

Sales activity was solid accounting for 55% of all transactions, this as a metric points to an extremely strong buying market. As mentioned in previous reports the supply of smaller factory unit developments is evident. The take up was equally noticeable with 78% of all factory sales being sub 300 m2. This is the highest percentage we have seen since commencing these reports and had the culminating effect of reducing our average sale price by 33% whilst increasing our average square metre sale rate by 28%.

Factory leasing was good and a push into the 1,000 m2 – 5,000 m2 band was encouraging. Average m2 rates pushed closer to the $90 m2 mark. Our thoughts about a supply side shortage of medium to larger new leasing stock is coming to fruition. Smart companies in need of larger premises are acting now before it tightens further.

Land sales were subdued limited purely by supply. Our figures are distorted by some larger broad acreage sales but generally we are seeing an aggressive increase in smaller retail lot pricing with $300 per m2 – $500 per m2 becoming the norm.

Investment yields continued compressing as investors hunted for returns frustrated by “Cash in Bank” rates.

Generally our market is holding together well and we look forward to the remainder of 2018.

As always this information is general in its format to provide a snap shot of overall conditions. Please give us a call to provide you with more detailed statistics and advice relevant to your specific requirement, development or investment.